.post-accordion-wrapper .accordion-content {

max-height: 0;

overflow: hidden;

}

For nearly 400 years, securities existed only in physical form. It wasn’t until the early 1990s that the digital era began, ushering in electronic registries and fully digitized trading.

Fast forward to 2025, and a relatively new idea is gaining serious momentum — the tokenization of stocks.

Until recently, tokenized equities were seen as a niche curiosity. But things have changed rapidly. Today, you can buy Apple or Tesla shares directly on a crypto exchange. The line between traditional finance (TradFi) and decentralized finance (DeFi) is growing ever thinner.

The idea of tokenized stocks is now widely discussed in the financial and crypto communities, which appear to be split into two camps. On one side are skeptics who question the viability of this concept. On the other are believers who see tokenization as a potential solution to the most pressing problems of today’s stock markets.

The Incrypted team took a deep dive into the world of tokenized equities — how they work, what benefits and risks they carry, and whether on-chain trading could truly disrupt the global financial system.

What Are Tokenized Stocks?

There’s no universally accepted classification for tokenized stocks yet, but they can generally be grouped into several categories.

Asset-Backed

Each tokenized stock is backed by a real asset held by a custodian. While this setup ensures that the token is collateralized, it also requires a high level of trust in both the issuer and the entity responsible for safeguarding the underlying shares.

One example of this model is xStocks by Backed Finance — a Swiss company that acts as both issuer and custodian. The tokens are backed by actual shares, and any dividends are automatically reinvested into the tokenized asset.

Since these tokens can be traded 24/7, while traditional stock exchanges operate on fixed schedules, price discrepancies can occur. During market hours, such gaps are usually corrected through arbitrage. But after hours, those divergences often persist until the next trading session.

Synthetic

Synthetic tokenized stocks are not backed by real shares. Instead, they use smart contracts and price oracles to mirror the value of an underlying asset. In many cases, users are required to lock up collateral — usually in stablecoins — to maintain price stability.

One example is Ostium, a platform built on Arbitrum that enables users to trade synthetic versions of traditional assets through perpetual futures.

Indirect Exposure via SPVs (private equity)

Robinhood recently announced support for tokenized assets tied to private companies like OpenAI and SpaceX.

These tokens aren’t actual shares and don’t carry legal shareholder rights. Instead, they’re backed by Robinhood’s ownership in a Special Purpose Vehicle (SPV) — a legal entity created specifically to hold equity in the private company.

This setup gives investors indirect exposure to pre-IPO companies. However, the structure relies on a relatively opaque SPV framework, which introduces both legal and regulatory risks.

Ownership in private companies is typically limited to closed investment rounds, venture capital funds, or specialized legal structures known as Special Purpose Vehicles (SPVs).

An SPV is a separate legal entity designed to isolate financial risk. Multiple investors can participate in an SPV to jointly hold assets such as stocks, bonds, or other securities.

According to Robinhood CEO Vlad Tenev, the platform acquires shares in private companies through SPVs and then issues tokens pegged to those holdings.

However, questions remain. It’s still unclear how Robinhood gains access to these private equity stakes — and there have been no public disclosures detailing the SPV structure or the legal framework surrounding ownership.

These “OpenAI tokens” are not OpenAI equity. We did not partner with Robinhood, were not involved in this, and do not endorse it. Any transfer of OpenAI equity requires our approval?we did not approve any transfer.

Please be careful.

— OpenAI Newsroom (@OpenAINewsroom) July 2, 2025

However, OpenAI stated that it does not endorse the launch of these tokens and is not affiliated with Robinhood’s initiative. In response, Vlad Tenev clarified that the tokens are not legally considered shares but do provide exposure to the securities of private companies.

.post-accordion-wrapper .accordion-content {

max-height: 0;

overflow: hidden;

}

Native

In this model, shares (or fractions of shares) are issued directly on the blockchain without duplication in traditional registries — the token itself is the security. This approach removes intermediaries and eliminates the need to reconcile data between the blockchain and external systems.

Issuing and managing such blockchain-based securities requires strict compliance with financial regulations. The issuer must ensure transparency of ownership, adhere to KYC/AML requirements, and complete necessary registration procedures.

A notable example is Exodus Movement Inc., the developer behind the Exodus crypto wallet. In June 2021, the company issued its shares as EXIT tokens on the Algorand blockchain via the Securitize platform.

Later, these securities started trading over-the-counter on the OTCQX market under the ticker EXOD, and from May 9, 2024, they were listed on the New York Stock Exchange (NYSE). On-chain trading of the tokens remains available through Securitize.

The variety of issuance methods highlights ongoing efforts to create efficient tokenization tools.

The motivation is clear — providers who can attract users from jurisdictions without direct access to the U.S. stock market stand to gain significant advantages.

But tokenization’s potential extends beyond this single challenge.

How Tokenization Addresses Traditional Market Challenges?

Conventional stock exchanges remain the backbone of the global financial system. However, this model comes with its limitations: fixed trading hours, numerous intermediaries, and delays in settlement processes.

Tokenization offers an alternative framework with several advantages — benefiting both investors and the financial system as a whole.

24/7 Stock Trading

One of the key reasons why tokenizing stocks matters so much is the ability to trade around the clock, without any time restrictions.

To buy shares of a public company, investors must consider the trading hours of the exchange where those shares are listed.

For example, Tesla stocks trade on the New York Stock Exchange (NYSE), where the trading session runs from 9:30 AM to 4:00 PM Eastern Time (ET), which is 1:30 PM to 8:00 PM in Kyiv.

There is no trading on weekends and public holidays. On certain days before holidays, the exchange may close early — for instance, on July 3, 2025, the session ended three hours earlier than usual, and on July 4, U.S. Independence Day, the markets were completely closed.

.post-accordion-wrapper .accordion-content {

max-height: 0;

overflow: hidden;

}

Tokenized stocks, on the other hand, can be bought and sold regardless of exchange hours. This is especially convenient for users in different time zones, allowing them to react in real-time rather than waiting for the market to open.

On Robinhood, tokenized stocks trade 24/5. xStocks tokens are available on some centralized exchanges (CEX) with similar time restrictions, but on decentralized exchanges (DEX), they can be traded around the clock.

Some platforms still align with traditional market hours. For example, Ostium does not allow trading synthetic stocks when traditional markets are closed. While orders can be placed outside of trading hours, they are only executed once the market opens and the target price is reached.

This limitation stems from technical reasons: oracles cannot provide up-to-date price feeds during off-hours, making accurate pricing impossible.

Additionally, when trading on Ostium with leverage of 10x or higher, positions are automatically closed 15 minutes before the session ends.

Asset Control and Management

In the traditional model, shares purchased by an investor are held in the broker’s account. Transferring these shares to a personal wallet or having full control over them is usually impossible — access is typically mediated by intermediaries.Tokenization changes this dynamic.

For example, xStocks tokens can already be withdrawn to personal wallets, and integrations with platforms like Raydium, Jupiter, and Kamino broaden their use cases. Meanwhile, Robinhood is building its own blockchain on the Arbitrum network to offer users new ways to manage their assets.

Global Access and Faster Settlements

On traditional stock markets, trades don’t settle instantly — they follow delayed settlement models like T+1 (the next business day) or T+2 (two business days later), depending on the jurisdiction.

In contrast, blockchain-based assets can be used immediately after purchase, without intermediaries or delays. This enables investors to react faster to price movements and manage their positions more flexibly.

Another major advantage is global accessibility. People from countries where working with traditional brokers is challenging can now acquire tokenized stocks via blockchain. This expands the investor base, simplifies capital raising, and boosts liquidity.

What was once exclusive to digital assets is now becoming a reality for securities. But is tokenization truly a breakthrough — or just an overrated trend?

What Supporters of Tokenization Say

Larry Fink, CEO of BlackRock, believes tokenization will radically simplify the financial system. In 2025, he compared SWIFT to the postal service and tokenization to email.

“Every stock, every bond, every fund — everything can be tokenized. And if that happens, investing will be changed forever,” he said.

Fink calls tokenization the “democratization of finance.” According to him, it opens access to fractional ownership, streamlines shareholder voting, and lowers barriers for participation in high-yield investments that were once reserved for large players.

He is confident that in the future, tokenized funds will become as commonplace as ETFs are today. However, scaling this model requires solving digital identity challenges — as has already been done in countries like India.

Using the Aadhaar system, India assigned a unique 12-digit number to the majority of its population. This number is linked to biometric data (fingerprints, iris scans, photos) and basic personal information (name, address, date of birth). On this foundation, India built a comprehensive digital identity system covering over 1.3 billion people.

With Aadhaar, citizens gained access to a wide range of services — from receiving subsidies and pensions to opening bank accounts. This approach reduced bureaucracy, lowered fraud, and enabled millions to use government services even in the most remote villages.

However, the system is not without flaws. There have been data leaks and technical glitches. Privacy activists have also raised concerns, as sensitive data of nearly the entire population is concentrated in a single database.

.post-accordion-wrapper .accordion-content {

max-height: 0;

overflow: hidden;

}

Meanwhile, U.S. Securities and Exchange Commission (SEC) Chair Paul Atkins has urged regulators not to hinder innovation. In a recent CNBC interview, he emphasized the agency’s role in supporting new formats, including the tokenization of securities.

A similar perspective is shared by Dinari co-founder Gabriel Otte. He believes tokenization of stocks can fundamentally transform traditional markets by reducing trading costs, speeding up settlements, and enabling 24/7 trading — unlike the limited hours of stock exchanges.

Otte is convinced that the next step is establishing a legal standard for tokenized stocks in the U.S. He calls this a necessary foundation for the future infrastructure, where not only brokers but also exchanges themselves will operate entirely on blockchain.

What Are the Challenges of Tokenization?

Rob Hadik, partner at Dragonfly Capital, takes a more cautious stance. He believes tokenized securities like xStocks are still far from perfect. Behind each token stands an SPV, not the actual shares themselves, and access to the asset is only possible after completing KYC procedures.

According to him, this creates liquidity issues. Over weekends, market makers bear the risk of price fluctuations because they cannot buy the real shares to hedge their positions. As a result, they widen spreads or sometimes halt trading altogether.

I know everyone is really bulled up on the Robinhood announcement and tokenized equities, and not to be a bear, but the conversation seems to lack a lot of nuance. I’m a long term bull but I expect near term expectations are WAY too high. So lets take a critical look.

So, how…

— Rob Hadick ?|? (@HadickM) July 1, 2025

Hadik argues that these products may only be useful for a small segment of investors — such as traders without access to traditional brokers. For now, tokenized stocks are not ready to serve institutional players and remain a transitional phase on the way to true tokenization, where major markets move onto blockchain and genuine liquidity emerges.

Meanwhile, Superstate believes the tokenized stock market is heading down the wrong path. Most of these instruments are mere “wrappers” created through third-party platforms or offshore SPVs, which do not confer real ownership.

This situation raises regulatory concerns. SEC Commissioner Hester Peirce emphasizes, that blockchain does not change the fundamental nature of the asset:

“Tokenized stocks are still securities.”

While Peirce generally supports innovation in crypto, she reminds that even digitized assets must comply with the same regulatory requirements as traditional stocks.

Joining the criticism is attorney Kurt Watkins, founder of the U.S. law firm Watkins Legal. He calls Robinhood’s OpenAI tokenization model opaque and unsafe for investors.

According to Watkins, the SPV structure does not grant real ownership rights, tokens may not reflect true market prices, and the investment itself appears illusory. Such a product, he argues, will not withstand regulatory pressure and is unlikely to be viable in the U.S. market.

Given such criticism, a reasonable question arises: is there real demand for tokenized stocks at all? To understand how viable these projects are, we need to look at the numbers.

Real Demand or Just Marketing?

According to RWA.xyz, as of July 22, 2025, the total market capitalization of tokenized stocks exceeds $528 million. Over 75% of this volume is concentrated in three assets — EXOD (mentioned earlier), Montis Group (MGL), and Backed CSPX Core S&P 500 (bCSPX).

The market leader by capitalization is EXOD, with a value of approximately $342 million. However, the spotlight in recent weeks has been on xStocks tokens, launched on June 30.

At the time of writing, the xStocks ecosystem hosts 61 assets and has recorded over 22,000 unique addresses interacting with the tokens. Since launch, the total trading volume has exceeded $65 million.

In the first days after launch, activity spikes were observed, but things soon stabilized. Peak interest occurred on July 2, when users traded $8.56 million. The most active tokens were SPYx, TSLAx, CRCLx, and MSTRx.

At the time of writing, daily trading volumes hover around $2–3 million, though they noticeably drop on Saturdays and Sundays. This is likely due to xStocks not being tradable on centralized exchanges (CEX) during weekends.

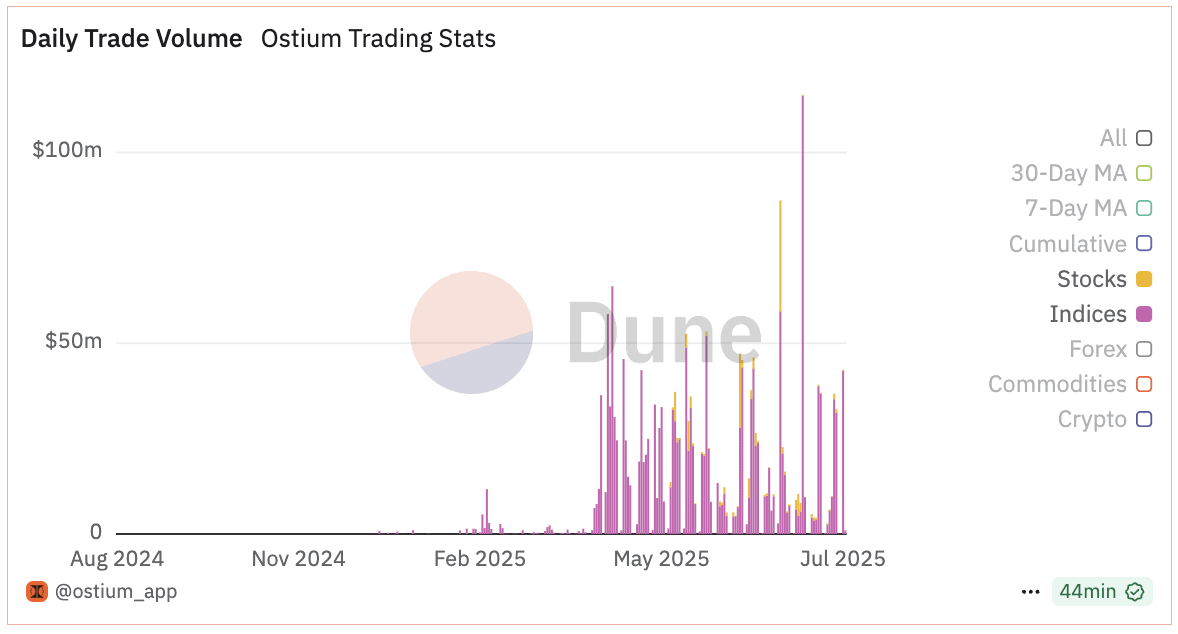

Another major player in this market is the Ostium platform, where synthetic stocks are traded. Since these tokens are not backed by real assets, Ostium does not appear in RWA.xyz’s statistics.

As of this writing, Ostium has over 10,000 registered users and a total of more than 200,000 unique trades.

The majority of trading volume on Ostium comes from indices — sometimes even surpassing cryptocurrency pairs. Meanwhile, stocks occasionally show spikes in activity — on June 23, the total trade volume reached around $29 million.

Despite active discussions, the actual volumes of tokenized stocks remain modest. There is interest in the topic, but in terms of numbers, it remains a niche segment with low liquidity and limited demand. The industry is still in its early stages, and it is too soon to talk about mass adoption or serious competition with traditional markets.

Segment Outlook

Tokenized stocks remain more of an experiment than a full-fledged alternative to traditional markets. Nonetheless, the technological foundation is already in place, and the segment continues to evolve.

The key question is institutional adoption. For tokenized stocks to truly scale, several challenges must be addressed:

- Simplifying user onboarding;

- Eliminating legal uncertainties;

- Ensuring stable liquidity;

- Building robust asset custody infrastructure — or issuing securities directly on the blockchain.

And that is exactly the direction the industry is heading. Robinhood is building its own blockchain, Backed Finance is expanding xStocks, Superstate is developing infrastructure for Opening Bell, and market interest is growing.

Analysts at Bitwise believe that even capturing 1-5% of the traditional stock and bond market in tokens could unlock access to trillions of dollars in investments.

By scale, this could surpass any other crypto use case. Following early initiatives like xStocks and Robinhood Chain, other major players are expected to join the segment. Bitwise anticipates a wave of new launches in the coming months.

If current growth continues, tokenized stocks may become a standard part of an investor’s portfolio. Over time, they might form the backbone of a new financial infrastructure. But to get there, the industry must travel a long road — from initial experimental launches to a mature ecosystem trusted by both retail users and institutions.